Loan Calculator

Enter Loan Amount, Interest Rate, and Term to calculate payments.

Debt Service Coverage Ratio (DSCR)

Measures how easily income covers debt payments.

Formula: DSCR = NOI ÷ Annual Debt Service.

Lenders typically require a DSCR greater than 1.25.

A higher DSCR indicates safer loan coverage and lower lender risk.

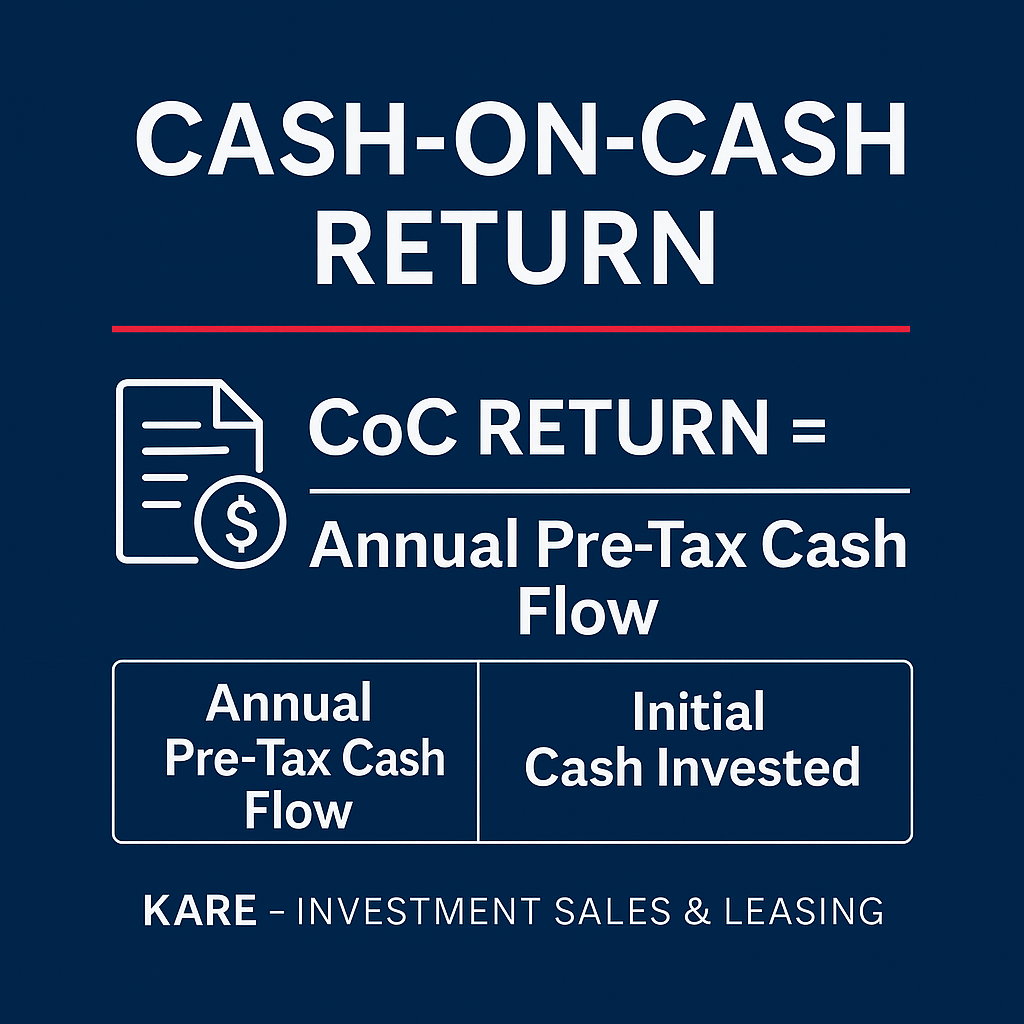

Cash-on-Cash Return (CoC)

Tracks return on the actual cash invested.

Formula: CoC = Annual Pre-Tax Cash Flow ÷ Initial Cash Invested.

Shows investor yield after financing is applied.

Quick way to evaluate equity performance.

Rent vs. Buy (for Businesses)

Compares the monthly rent cost to the mortgage payment.

Formula: Rent = Lease Rate × Size ÷ 12; Buy = Loan Payment

Helps businesses decide between leasing and ownership.

Buying builds equity, while renting preserves flexibility.

FAQ

How is this calculator useful for commercial real estate?

It helps investors and business owners quickly estimate debt service on a property purchase. By knowing the monthly payment and total interest, you can better evaluate if a deal fits your investment goals.

Does this calculator include DSCR or other lending metrics?

The Loan Calculator itself shows principal and interest payments.

What inputs do I need to use the calculator?

Simply enter the loan amount, interest rate, and loan term. The calculator will automatically estimate monthly payments, total interest, and total repayment cost.

Why is the Debt Service Coverage Ratio (DSCR) important?

In commercial real estate, lenders look beyond the property value; they want to ensure the property’s net income covers the debt. A DSCR of 1.25 or higher is generally required.

Can I use this calculator for SBA, bridge, or construction loans?

Yes, it works for any loan where you want to estimate payments based on amount, rate, and term. Keep in mind that certain loan products may have variable rates, interest-only periods, or balloon payments that are not reflected here.

Does this tool account for operating expenses, taxes, or insurance?

No, it strictly calculates debt service (principal and interest). For a complete financial picture, combine it with your property’s Net Operating Income (NOI) and expense estimates.

Is this calculator a substitute for lender underwriting?

No,it’s an investor planning tool. While it provides reliable estimates, final terms, covenants, and qualifications depend on the lender’s underwriting process.

What’s the difference between a 20-year and 30-year amortization in CRE loans?

Shorter amortizations mean higher payments but faster equity build-up and less interest. Longer amortizations lower the monthly debt service, but total interest is higher. Many CRE loans use 20–25-year schedules.

What does Cash-on-Cash Return measure?

Cash-on-Cash Return (CoC) measures the annual pre-tax cash flow a property generates compared to the total equity you invested (down payment + closing costs + initial improvements).

Why is CoC important in commercial real estate?

Unlike the Cap Rate, which ignores financing, CoC shows the actual return on your invested cash. It’s one of the fastest ways to evaluate whether a property is performing well for equity investors.

How is CoC different from Cap Rate?

Cap Rate looks only at property income versus price, ignoring financing. CoC factors in leverage (loan terms), showing the real return on your cash out of pocket.

Why compare renting and buying for my business?

Renting offers flexibility and lower upfront costs, while buying can build long-term equity and stability. This calculator helps you see which option makes more financial sense for your situation.

What costs are included in the calculator?

The Rent side factors in the annual lease rate and space size. The Buy side estimates mortgage payments based on loan amount, interest rate, and term. For a full picture, you should also consider taxes, insurance, and maintenance costs.

When does buying usually make more sense?

Buying is often better for businesses planning to stay long-term, wanting to control occupancy costs, and seeking to build equity through real estate ownership.

When is renting better?

Renting may be better if your business needs flexibility, expects to grow or downsize soon, or wants to avoid the responsibilities of property ownership.

Can I use this calculator to secure financing?

No, it’s a decision-making tool. For financing options, you’ll still need to speak with lenders, who will consider additional factors like DSCR, creditworthiness, and property type.

Disclaimer

This tool is for educational purposes only and does not constitute an appraisal, valuation opinion, or investment advice. Figures are estimates based on user inputs and indicative market ranges.Actual financing terms, operating results, and investment performance will vary based on lender underwriting, market conditions, and property-specific factors. Users are solely responsible for verifying all calculations and assumptions before making any investment or financing decisions.KARE – Investment Sales & Leasing makes no warranties or representations regarding the accuracy, completeness, or suitability of these tools for any particular use. Please consult with qualified professionals (lenders, accountants, attorneys, or financial advisors) before acting on the results generated by these calculators.