The Texas Advantage

Texas outperforms national benchmarks on population growth, job creation, and logistics capacity. Over the past five years, population and job growth have exceeded the U.S. average, supporting durable space demand across industrial, office, retail, land, and multifamily. Industrial vacancy typically runs below the national average, retail availability is tighter, multifamily rent growth is stronger in leading metros, and the share of office sublease space is more manageable than in many coastal markets. Cap rates generally price wider than in coastal gateway markets, creating attractive risk-adjusted yields. Operating conditions include no state income tax and a regulatory climate that supports speed to market. A central location with Interstates 35, 10, and 45, Gulf Coast ports, Class I rail, and Tier 1 air cargo hubs expands customer reach and shortens delivery times.

Industrial

Sales Market

Activity is steady but selective, with pricing clearly bifurcating by functionality and location. Infill shallow-bay trades faster with stronger owner-user and private-capital demand, while older or less functional assets face wider discounts and longer timelines. Institutional capital remains focused on best-in-class logistics and strong credit.

Median sold price $415.3K; median building size 6,519 SF; median $/SF $50; median cap rate 7.3% (asking/sold); median year built 1984; median DOM 228; median site size 1 acre.

Lease Market

Demand is balanced in shallow-bay last-mile and light-manufacturing space, while larger boxes vary by corridor and near-term supply. Face rents are broadly stable, with targeted concessions where new deliveries cluster. Tenants prioritize move-in readiness, clear height, loading, reliable power, and yard/parking.

Median quoted rate $12/SF (Annual); median lease term 5 years; median space size 6,003 SF; median DOM 321.

Our Take

Price and position by functionality + access, not vintage. If you’re leasing, deliver spec suites and spotlight loading, power, and yard to cut time-to-revenue. If you’re selling, lead it with operational features and interstate/arterial access, and price non-functional buildings realistically to keep momentum.

Office

Sales Market

Trading is selective with clear separation by building quality, location, and readiness. Smaller professional and medical offices see steadier activity, while older commodity assets need sharper pricing and a clear repositioning story. Buyer mix skews to owner users and private capital; institutions focus on best located, well-leased assets.

Median sold price $544.4k; median building size 4,355 SF; median $/SF $124; median cap rate 7.0 percent (asking and sold); median year built 1985; median DOM 219; median site size 1 acre.

Lease Market

Demand concentrates in amenitized Class A and Class A–B nodes and in efficient suburban low-rise with good parking. Spec suites and flexible layouts shorten decision time. Concessions are used where new supply or large blocks compete, but face rates remain stable in the strongest corridors.

Median quoted rate $2.00/SF per month (about $24/SF per year); median lease term 5 years; median space size 2,134 SF; median DOM 391.

Our Take

Lead with convenience, amenities, and efficiency. For leasing, deliver move-in-ready spec suites, highlight parking ratios, natural light, and proximity to rooftops and services, and price with clarity on concessions and TI. For sales, focus on location quality, tenant durability, and a simple plan to improve occupancy or rollover terms. Where vintage is older, frame a practical reposition path and price to clear in today’s underwriting.

Retail

Sales Market

Transaction flow is steady and driven by neighborhood centers, outparcels, and credit STNL, with pricing separated by tenant quality, lease term, and location fundamentals. Grocer-anchored and daily-needs strip centers remain liquid; older centers without a clear re-merchandising plan require sharper pricing.

Median sold price $524.9K; median building size 4,059 SF; median $/SF $112; median cap rate 6.3% (asking) / 6.2% (sold); median year built 1987; median DOM 190; median site size 1 acre.

Lease Market

Demand concentrates in pad sites and service/medical retail. Construction remains disciplined, supporting headline rents; concessions show up in weaker corridors or larger vacancies. Visibility, access, parking, and co-tenancy drive decision speed.

Median quoted rate $2.00/SF per month (~$24/SF annual); median lease term 10 years; median space size 2,279 SF; median DOM 366.

Our Take

Lead with location and tenant durability. For leasing, prioritize visibility, signage, traffic counts, and quick-start suites to shorten downtime. For sales, frame it around credit, remaining term, rent sustainability, and a simple re-merchandising plan where needed; price older centers realistically unless there’s clear upside from turnover or outparcel activation.

Multifamily

Sales Market

Trading is active across small multi (2–10 units), B/C garden assets, and newer suburban product, with pricing set by location, school districts, and rent sustainability. Private buyers and 1031 exchanges lead most transactions; syndicators focus on clear value-add in rising submarkets. Cap-rate expectations widen for older assets without proven rent lift or with high insurance/tax loads.

Median sold price $525k; median building size 4,147 SF; median $/SF $143; median cap rate 7.4% (asking) / 7.7% (sold); median year built 2007; median DOM 181; median units 4; median price per unit $110.7k.

Our Take

Durable renter demand, realistic current rents, and a clear path to operational improvements. Underwrite taxes, insurance, and turn costs conservatively; verify utility capacity and any deferred maintenance early. Where supply is heavy, assume modest rent growth and focus on management execution (unit turns, marketing, resident retention). In rising corridors, emphasize walkability, schools, and access to jobs to support rent and occupancy stability.

Need a concise, property-specific market report? Get a clear summary of current pricing, recent sales and leasing comps, cap-rate context, and submarket trends so you can make decisions with confidence. Click below to order your report.

Major Developments Shaping Texas

Samsung Semiconductor Plant – Taylor, Texas

A cornerstone of Texas’ advanced manufacturing expansion, Samsung’s $17 billion semiconductor facility in Taylor spans more than 1,000 acres and will produce cutting-edge logic chips for global supply chains. The project includes over 6 million SF of cleanroom, R&D, and support space, with operations expected to begin in 2026. Once complete, it’s projected to create 2,000+ direct jobs and anchor a new regional technology corridor northeast of Austin.

Rio Grande LNG – Brownsville, Texas

Rio Grande LNG in Brownsville, developed by NextDecade, is a major Gulf Coast export terminal on the Brownsville Ship Channel. Phase 1 includes three liquefaction trains targeting ~17–18 MTPA, with full buildout envisioned in the mid-20s MTPA. The project reached FID in 2023; Bechtel is the EPC and construction is mobilized while agencies complete a supplemental environmental review following a 2024 court remand. Feedgas will be supplied via the Rio Bravo Pipeline (now owned by Enbridge). NextDecade has withdrawn the on-site CCS concept and is emphasizing lower-carbon LNG sourcing. Once operational, the facility is expected to be among Texas’s largest LNG hubs, supporting thousands of construction jobs and long-term port activity in the Rio Grande Valley.

UT Southwestern Pediatric Campus – Dallas, TX

UT Southwestern and Children’s Health are constructing a $5B pediatric health campus in Dallas’ Southwestern Medical District, directly across from UTSW’s Clements University Hospital at Harry Hines Blvd. and Paul M. Bass Way. The ~4.7M SF build centers on a new hospital with two 12-story towers and one eight-story tower, delivering 552 beds (about a 38% increase) with room to expand. Ground broke on October 1, 2024, with opening targeted in roughly 6–7 years (around 2031). Program highlights include expanded emergency and surgical capacity, a Level I pediatric trauma center, two helipads, and a new fetal care center. The project is supported by significant philanthropy, including a major gift from the Moody Foundation.

Texas Heritage Marketplace – Katy, TX

A ~$400M, 165-acre mixed-use destination by NewQuest at the SE corner of I-10 & Texas Heritage Parkway (Waller County). Plans call for ~750,000 SF of retail/dining anchored by a 148–149k SF Target (targeting 2026 openings), ~300,000 SF of medical office/self-storage, and ~550 apartments delivering in phases through 2028. A five-acre central green organized around a preserved heritage oak is designed as the project’s community hub; site and utility work kicked off with vertical construction following in 2025.

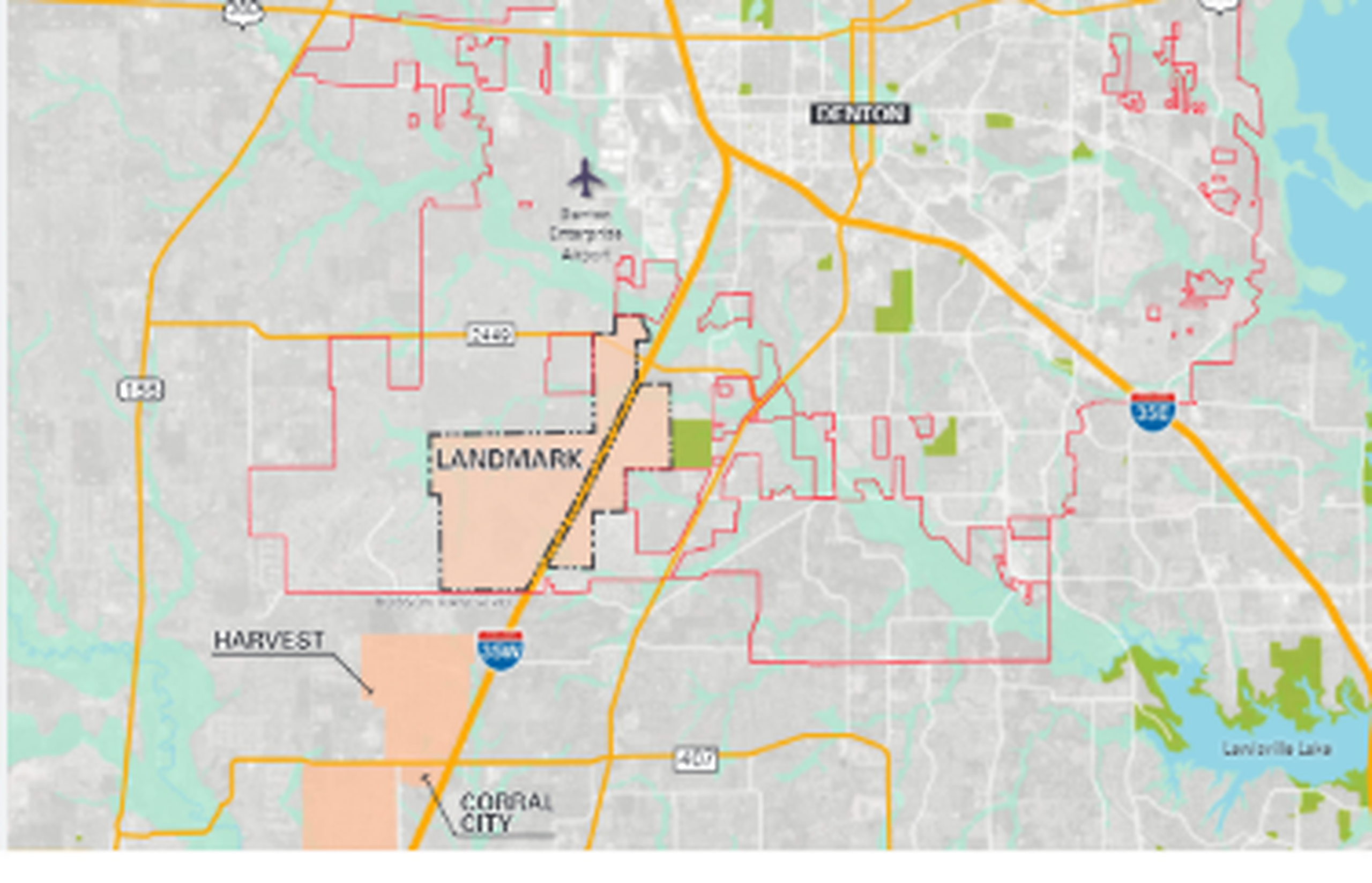

Hillwood Landmark Mixed-Use Development – Denton County, TX

Landmark by Hillwood is a 3,200-acre master-planned community at I-35W & Robson Ranch Rd. planned for ~6,000 single-family homes, 3,000+ multifamily units, and ~5M SF of commercial/mixed-use space, plus ~1,100 acres of parks, trails, and open space. Early site and lot work began in 2024/2025, with initial commercial anchored by a planned H-E-B at the northwest corner of I-35W and Robson Ranch. Positioned as a southern gateway to the AllianceTexas corridor, the project extends Hillwood’s long-range Denton County footprint and is designed as a live-work-play district integrated with significant natural amenities.

Sachs on the Seawall -Galveston, TX

Sachs on the Seawall is a $540 million mixed-use coastal development planned along Galveston’s Seawall Boulevard near 45th Street. Developed by the Sachs Company, the project will feature a 216-room luxury hotel, two condominium towers, two apartment towers, and several restaurants and retail spaces with walkable public areas. The design includes about four acres of landscaped green space overlooking the Gulf, enhancing both public access and the city’s tourism appeal. Construction is expected to begin in late 2025, with phased completion through 2029. Once finished, it will stand as one of Galveston’s largest private investments, bringing significant hospitality, residential, and retail opportunities to the area.

Tesla Gigafactory Texas -Travis County

The Tesla Gigafactory in Travis County, also known as Giga Texas, is one of Tesla’s largest and most advanced production facilities worldwide. Spanning over 10 million square feet on a 2,500-acre site along the Colorado River near Austin, the factory serves as the central hub for manufacturing the Model Y, Cybertruck, and upcoming Tesla Semi. The project represents more than $5 billion in investment and employs tens of thousands of workers, with continued expansion underway. Current additions include a battery cathode facility, logistics park, and advanced testing center aimed at improving efficiency and in-house battery production. Beyond its scale, the Gigafactory has fueled economic growth throughout Central Texas, transforming the Austin–Bastrop corridor into a growing hub for clean energy and high-tech manufacturing.

Castle Hills – Lewisville, Texas

Castle Hills is transforming from a suburban neighborhood into a self-contained urban district, designed to let residents live, work, and play within one community.

Its mix of modern office spaces, multifamily housing, and entertainment venues positions it as a major suburban employment and lifestyle hub in the North Dallas corridor, rivaling areas like Legacy West and Cypress Waters.

The community’s success has also driven significant land value appreciation and continues to attract both corporate tenants and high-income residents, making it one of the most dynamic suburban developments in North Texas.

Disclaimer

The information provided on this Market Insights page is for general informational purposes only. While KARE Investment Sales & Leasing strives to present accurate and up-to-date market data, all information is subject to change without notice and may include content from third-party sources deemed reliable but not guaranteed.

KARE Investment Sales & Leasing makes no representations or warranties regarding the completeness or accuracy of the information presented. Readers should conduct their own due diligence and consult qualified professionals before making any investment, purchase, or leasing decisions.

Work With Us

.